Following continued

declining natural gas production and a 2018 ban on offshore drilling, New

Zealand is moving back towards natural gas. Both new drilling and LNG imports

are expected to occur as the 2018 ban is lifted and LNG has been given consent

by the center-right government. Reuters reports that according to New Zealand’s

energy minister “natural gas production fell by 12.5% in 2023 and a further

27.8% in the first three months of 2024, triggering a nationwide energy

shortage as generators switched to more coal and diesel to power the grid.”

The Taranaki Basin: Main Source of New Zealand Natural

Gas and Oil

The Taranaki

Basin is a Cretaceous rift basin on the West Coast of New Zealand that extends

both onshore and offshore. Extensional stresses during the breakup of

Gondwanaland led to the rifting. Production from the basin makes up the

majority of New Zealand’s hydrocarbons. 70% of the production is natural gas. The total reserves discovered are about 1.8 billion barrels of oil equivalent (BOE). Around

400 wells have been drilled in about 20 fields. Due to the complex history of the basin, there are several different kinds of plays and traps, mostly

structural. Cretaceous marine shales and coals are the source rocks. The

multitude of play and trap types and the small number of wells drilled suggest

that there are more hydrocarbons to be found in the basin. Structural play types

include thrust fault traps, inversion structures, extensional structures,

half-graben fills, stratovolcano flank traps, submarine fans, and

diagenetically altered sandstones. The variability in play types, trap types,

and rock mechanics means that each field may be much different. As can be seen

on the maps the fields tend to be small and discontinuous.

A 1997 article by

Richard Cook and Roger Gregg in the Oil & Gas Journal describes the geologic

setting in terms of tectonics and stratigraphy for the Taranaki Basin:

1. Late Cretaceous to Paleocene intra-continental rift

transform, characterized by nonmarine sedimentation in restricted,

fault-controlled basins. These sediments include important coal measure source

rocks.

2. Eocene to Early Oligocene passive margin, associated

with post-rift thermal contraction and regional subsidence. Basinwide

sedimentation patterns were characterized by comparative tectonic quiescence,

peneplanation, and marine transgression. Coal measures and well developed

sandstones in the marginal marine setting contain proven source and reservoir

rocks.

3. Oligocene to Recent pericratonic basin, straddling the

outer limit of broad-scale deformation associated with the evolution of the

Australia-Pacific convergent plate boundary through New Zealand. Throughout the

Neogene, the basin has been part of the Australian Plate, and evolved with two

tectonic settings: active margin (Eastern mobile belt) and passive margin

(Western stable platform).

Maui Offshore Gas Field: Once the Biggest Field, It is

Now Depleted

The offshore Maui

gas field offshore of the North Island in the Taranaki Basin began full

production in 1979. Two platforms were operated. By 2005 it was considered over

90% depleted and production has dropped off considerably as seen below. However,

in 2014, reserves for the field were recalculated, suggesting there is more gas

to be produced. By a wide margin, the Maui field had the highest ultimately

recoverable reserves of both oil and gas. However, its remaining reserves are

now thought to be much smaller than most other fields. In an exploration sense,

finding another Maui field or two in the Taranaki Basin area would be a

solution to the dilemma.

Gas Production Decline

New Zealand’s natural

gas production is expected to drop below demand very soon. It is expected to be

about 10 petajoules (PJ) below the total demand of about 150 PJ for the next three years.

Usable gas reserves for the country are estimated at just 8.7 years. New

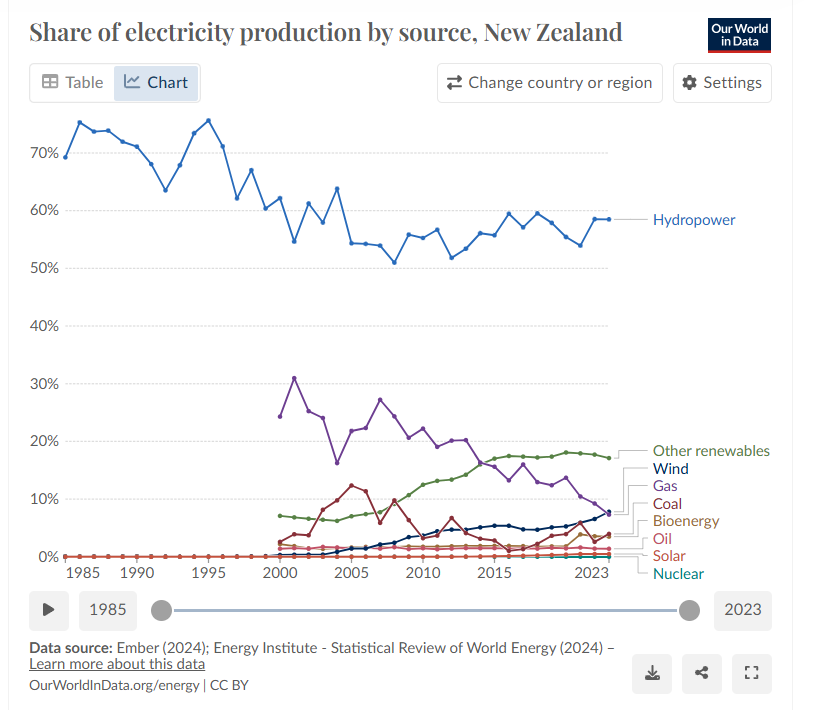

Zealand mainly relies on hydro (~60%), geothermal (~15%), and natural gas (~9%)

for electricity. Wind and solar are minor sources but are growing. Natural gas

is also used in industry, particularly the chemical industry. The gas shortage

is already affecting some industrial users. Most of the drop in estimated reserves

is due to use through time but over half is due to a recent re-evaluation by field

operators who adjusted reserves downward by about 185 PJ or about 1.25 of

usable reserves. In any case, this is quite concerning for anyone depending on

natural gas. It is an unsustainable situation. The Ministry of Business,

Innovation, and Employment reports:

“Of all the gas used in New Zealand in 2023, the majority

was used by the industrial sector, either being burned for heat (35% of all

use) or being used as a feedstock (26%) in factories. Around 29% of gas use was

for electricity generation, and the remaining 10% of use represented use by

households, schools, hospitals, and other businesses.”

New Zealand’s Primary Energy Use by Source and

Electricity Mix

Below are some graphs showing New Zealand’s primary energy use by source and its electricity mix by source. These are from the New Zealand government, Our World in Data, and Energy Institute's Statistical Review of World Energy.

The 2018 Offshore Ban and Its 2024 Lifting: Will Companies

Drill?

Jacinda Ahern’s

left-leaning government enacted a ban on offshore drilling in 2018. Companies have

been increasing spending and drilling development wells in New Zealand, but the

new wells have not performed well. It was originally hoped that the

weather-based renewables: solar, wind, and especially hydro, would make up any

shortfalls in the power sector, but that has not happened. Hydro has been impacted

by low water levels. Solar and wind have been underperforming as well. Electricity

prices have risen due to the gas shortage.

Now in 2024,

the cabinet of the government has agreed on some changes including lifting the

2018 ban and giving consent to build a new LNG import facility, which would be

the first in the country. Perhaps, if they had continued exploration and

drilling at pre-ban levels, they could have staved off the need to import LNG. Importing

LNG is significantly more carbon intensive than producing domestic gas and

pipelining it to where it is needed. It is yet another case in which environmentalism and climate change-influenced policies will likely lead to

more emissions than if the policy was never enacted. Fast-tracking permits are

also on the table, not only for natural gas development and the LNG terminals but also for renewables permitting and development.

Since most of New Zealand’s gas has come from offshore, the ban was immediately impactful. Not only was exploration banned by development drilling to extend fields was too. The ban did exclude a part of the area off of the west coast of the North Island in Taranaki. The ban reversal was strongly condemned by environmental groups and the country’s Green Party. In the past, climate activists and Greenpeace have targeted offshore drilling in New Zealand.

As noted, new exploration and spending on new wells failed to increase supply in recent years. Below is an analysis of cost and supply increases from 2016-2020 and 202-2024 showing the particularly poor results in the past four years. Significantly more gas was found at less than 30% of the cost in 2016-2020 compared to 2020-2024.

An Exploration Opportunity?

The previous

ban suggests that if a left-leaning government returns to power, the ban could

be re-enacted, leaving explorers stranded in monetizing the resources in which they

have invested. This creates regulatory uncertainty. However, with a clear gas

shortage that is affecting gas prices and electricity prices, there is a clear

need to increase natural gas supply.

These types

of structural plays require significant exploratory spending with extensive seismic

surveying and geologic modeling. Building new drilling and production platforms

is also time-intensive. Thus, exploring for, drilling, and producing new wells

is likely to take longer than building a new LNG import facility, which could

be built adjacent to an existing offshore platform.

It remains to

be seen if and when exploratory drilling will increase as a result of the ban

being lifted, but it is likely to happen.

References:

Govt

to automatically consent natural gas import facility. Marc Daalder. Newsroom.

August 26, 2024. Govt

to automatically consent natural gas import facility - Newsroom

NZ is

running out of gas – literally. That’s good for the climate, but it’s bad news

for the economy. David Dempsey, Jannik Haas, and Rebecca Peer. The

Conversation. August 12, 2024. NZ

is running out of gas – literally. That’s good for the climate, but it’s bad

news for the economy (theconversation.com)

Oil

and gas industry in New Zealand. Wikipedia. Oil

and gas industry in New Zealand - Wikipedia

Gas

Statistics. New Zealand Ministry of Business, Innovation, and Employment. Gas

statistics | Ministry of Business, Innovation & Employment (mbie.govt.nz)

Petroleum

in New Zealand. New Zealand Petroleum and Minerals. Petroleum in New

Zealand - New Zealand Petroleum and Minerals (nzpam.govt.nz)

New

Zealand to Reverse Oil and Gas Exploration Ban, Ease LNG Import Rules. Pipeline

& Gas Journal. August 26, 2024. New

Zealand to Reverse Oil and Gas Exploration Ban, Ease LNG Import Rules |

Pipeline and Gas Journal (pgjonline.com)

From

wellhead to burner - The New Zealand Gas Story, Gas Industry Company Limited. August

2014. https://www.gasindustry.co.nz/assets/DMSDocumentsOld/speeches/4488nz-gas-story-presentation-wellington-7-august-2014.pdf

Our

Energy Mix. Energy Resources.org. Our

Energy Mix | Energy Resources Aotearoa

The

Importance of Oil and Gas to New Zealand. Energy Resources.org. The

Importance of Oil & Gas to the New Zealand Economy (energyresources.org.nz)

New

Zealand: Energy Country Profile. Hannah Ritchie and Max Roser. Our World in

Data. New

Zealand: Energy Country Profile - Our World in Data

Overview

of New Zealand's petroleum systems, potential. Oil & Gas Journal. January

6, 1997. Overview

of New Zealand's petroleum systems, potential | Oil & Gas Journal (ogj.com)

Geology

of New Zealand. Wikipedia. Geology of New

Zealand - Wikipedia

Taranaki

Basin. Wikipedia. Taranaki

Basin - Wikipedia

Maui gas

field. Wikipedia. Maui

gas field - Wikipedia

Gas

production forecast to fall below demand. New Zealand Ministry of Business,

Innovation, and Employment. July 11, 2024. Gas

production forecast to fall below demand | Ministry of Business, Innovation

& Employment (mbie.govt.nz)

Electricity

sector in New Zealand. Wikipedia. Electricity

sector in New Zealand - Wikipedia

New

Zealand Petroleum Basins. New Zealand Petroleum and Minerals. Part 1. New

Zealand's Petroleum Basins - Part One (nzpam.govt.nz)

New

Zealand Petroleum Basins. New Zealand Petroleum and Minerals. Part 2. New

Zealand's Petroleum Basins - Part Two (nzpam.govt.nz)

Bill

to resume oil and gas exploration set for later this year. RNZ. June 9, 2024. Bill

to resume oil and gas exploration set for later this year | RNZ News

The

end of offshore oil and gas exploration in NZ was hard won – but it remains

politically fragile. The Conversation. May 8, 2023. The

end of offshore oil and gas exploration in NZ was hard won – but it remains

politically fragile (theconversation.com)

No comments:

Post a Comment