A few of my colleagues in the oil & gas industry have recently reiterated that drilling in the U.S. is not expected to pick up this year. I would have thought that it would pick up soon due to more LNG being exported and increased demand due to AI data centers. That may still happen but right now it doesn’t appear likely in 2025, perhaps in 2026, or maybe 2027.

Trump recently

conveyed to Saudi Arabia that he would like to see oil prices in the $45/barrel

range. As a buyer of gasoline, I would love that, but oil producers would be

hurt very badly by such pricing. Saudi Arabia is no longer the world’s swing

oil producer but with the full OPEC plus, they still have considerable leverage.

Of course, U.S. WTI pricing is typically lower than Brent international pricing

and Canadian crude is even cheaper than U.S. crude due to its quality.

$45/barrel would sink a lot of oil producers since that is below breakeven on

several important oil plays. That would bring pricing down to COVID levels and

we can see in the graph below from NOVI Labs where pricing and horizontal

drilling were then and since then.

Chevron just

announced a plan to lay off 15-20% of their global workforce, up to 9000

people. According to Reuters:

“Chevron is taking action to simplify our organizational

structure, execute faster and more effectively, and position the company for

stronger long-term competitiveness,” said Mark Nelson, vice chairman of

Chevron, in a statement. “We do not take these actions lightly and will support

our employees through the transition.”

BP has just come

under the influence of an activist investor who is focused on shareholder

value.

“We now plan to fundamentally reset our strategy and

drive further improvements in performance, all in service of growing cash flow

and returns,” CEO Murray Auchincloss told the Wall Street Journal a day after

news broke that activist investor Elliot Investment Management had purchased a

major position in the company’s stock.

The investment company has a reputation for making radical

changes to increase value for shareholders.

“In the letter, we would expect Elliott to illustrate

both BP’s alleged shortcomings and a clear path to increase value (likely

through some combination of reorganisation/cost reductions, divestment(s),

significant debt reduction)," Read said. "Following those efforts,

Elliott would likely expect BP to return significant cash to shareholders.”

BP has been plagued in recent years by safety issues,

including the 2010 Deepwater Horizon disaster. It has also indulged in unprofitable

investments in solar and wind in service to the energy transition. Other major

oil companies that have invested less in renewables have fared much better. BP

has managed to reduce its exposure to unprofitable wind and solar ventures and

to refocus more on oil and gas projects. Forbes writer David Blackmon thinks it

is possible that the activist investors will break up the company into pieces,

making it easier for a more profitable competitor like Shell to scoop them up. BP

also has plans to lay off 5% of its global workforce, up to 7700 people (if my

sources are correct).

Since Trump won

the election, other companies have announced layoffs including Equinor and

ExxonMobil, although the ExxonMobil layoffs may be due to the closing of their California

refinery. Before Trump was elected, other companies announced layoffs,

including EQT, Chesapeake Energy (now Expand Energy), and Enbridge.

I have spent

nearly 32 years working for the oil & gas industry through most of 2023

and I do not expect any job opportunities in the near future. Doing more with

less is the cornerstone of efficiency and perhaps optimizing shareholder value.

However, people need jobs too and there are many qualified people who have

given up and moved on, me included. I do believe that more LNG exports in

particular will spur some natural gas drilling, perhaps in 2026 and beyond, but

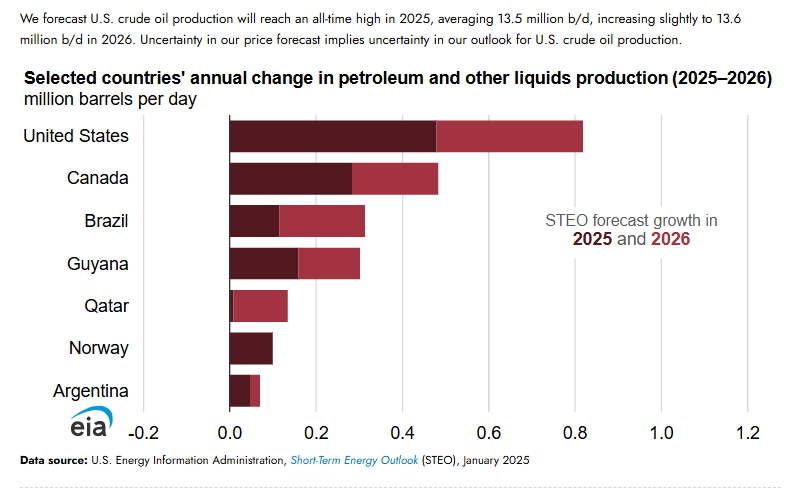

oil demand is not expected to rise. The EIA does predict slight increases in

oil production for the U.S. and Canada in 2025 and 2026 but prices are expected

to drop.

“We forecast benchmark Brent crude oil prices will fall

from an average of $81 per barrel (b) in 2024 to $74/b in 2025 and $66/b in

2026, as strong global growth in production of petroleum and

other liqyuds and slower demand growth put downward pressure on prices and

help offset heightened geopolitical risks and voluntary production restraint

from OPEC+ members.”

“Ultimately, we expect lower prices will reduce drilling

activity and investment in U.S. production of crude oil and other liquids,

leading to a small increase in production in 2026.”

Those price predictions do not bode well for a drilling

boom.

References:

BP

Promises Big Changes After Attracting An Uninvited Guest. David Blackmon. Forbes.

February 11, 2025. BP

Promises Big Changes After Attracting An Uninvited Guest

Chevron

to lay off 15% to 20% of global workforce. Reuters. February 12, 2025. Chevron

to lay off 15% to 20% of global workforce | CNN Business

Complete

List of Recent Oil and Gas Layoffs. Usearch. Complete List of Recent

Oil and Gas Layoffs - Usearch

EIA

forecasts lower oil price in 2025 amid significant market uncertainties. EIA. Short

Term Energy Outlook. January 21, 2025. EIA forecasts

lower oil price in 2025 amid significant market uncertainties - U.S. Energy

Information Administration (EIA)

No comments:

Post a Comment